Key information

The fund invests primarily in equities that are directly or indirectly involved in agriculture or the food value chain. The asset allocation is managed independently of any benchmark constraints and the investment level can be reduced to 51% in difficult periods. Agricultural and food companies are expected to benefit from the structurally rising world population and drive long-term value appreciation. However, in the short term significant price fluctuations in agricultural commodities are possible. The fund refrains from investing in physical commodities or any derivatives, which benefit from rising food prices.

Responsible manager since inception

Key information

| ISIN: | LU0350835707 |

| WKN: | A0NGGC |

| Category: | Fund Sector Equity Agriculture |

| VG/KVG: | DJE Investment S.A. |

| Fund Management: | DJE Kapital AG |

| Risk Category: | 4 |

| This sub-fund/fund promotes ESG features in accordance with Article 8 of the Disclosure Regulation (EU Nr. 2019/2088). | |

| Type of Share: | |

| Financial Year: | 01.01. - 31.12. |

| Launch Date: | 02/06/2008 |

| Fund Currency: | |

| Fund Size (18/04/2024): | 30,23 Mio |

| TER p.a. (29/12/2023): | 2,06 % |

| Reference Index: | - |

Fees

| Initial Charge: | 5,000 % |

| Management Fee p.a.: | 1,650 % |

| Custodian Fee p.a.: | 0,060 % |

|

Performance Fee p.a.: 10% of the [Hurdle: exceeding 6% p.a.] unit value performance, provided the unit value at the end of the settlement period is higher than the highest unit value at the end of the previous settlement periods of the last 5 years [High Water Mark Principle]. The settlement period begins on 1 January and ends on 31 December of a calendar year. Payment is made at the end of the accounting period. For further details, see the sales prospectus. |

Ratings & Awards (18/04/2024)

| Morningstar*: |

|

|

Awards: €uro Eco Rating A Finanzen Verlag, Mountain View Q3 2023 |

All ESG information presented here relates to the fund portfolio shown and is sourced from MSCI ESG Research, a leading provider of environmental, social and governance analysis and ratings.

| MSCI ESG RATING (AAA-CCC): | AA |

| ESG-Qualityrating (0-10): | 7,990 |

| Environment Rating (0-10): | 5,389 |

| Social Rating (0-10): | 5,540 |

| Governance-Rating(0-10): | 6,722 |

| ESG rating in comparison group (0% lowest, 100% highest value): | 100,000 % |

| Peergroup: |

Equity Theme - Agribusiness

(36 Fonds) |

| Coverage rate ESG rating: | 97,718 % |

| Weighted average CO₂ intensity (tons of CO₂ per 1 million US dollars in sales): | 212,225 |

Portfolio allocation according to ESG rating of individual securities

Report date: 28/03/2024

- is proprietary to Morningstar and/or ist content providers may not be copied or distributed and is not warranted ob e accurate, complete or timely. Neither Morningstar nor ist content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

Perfomance Chart

Performance in Percent

Risk metrics (18/04/2024) |

|

|---|---|

| Standard Deviation (2 years): | 9,76 % |

| Tracking Error (1 years): | - |

| Value at Risk (99% / 20 days): | -6,67 % |

| Maximum Drawdown (1 year): | -6,55 % |

| Sharpe Ratio (2 years): | -1,23 |

| Correlation (1 years): | - |

| Beta (1 years): | - |

| Treynor Ratio (1 years): | - |

Top Country Allocation (28/03/2024) |

|

|---|---|

| United States | 28,63 % |

| Switzerland | 8,11 % |

| Japan | 7,53 % |

| United Kingdom | 7,31 % |

| Canada | 5,64 % |

Asset Allocation (28/03/2024) |

|

|---|---|

| Stocks | 93,61 % |

| Cash | 6,39 % |

Investment strategy

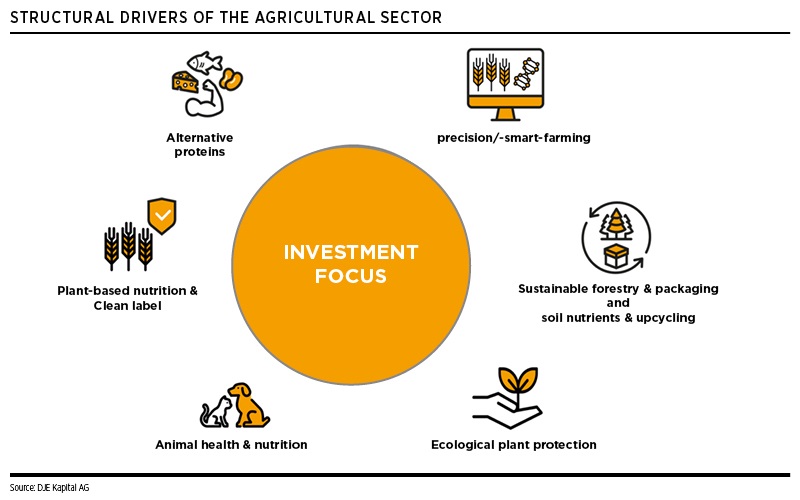

Aside from world population growth, the increasing demand for protein-rich foods resulting from rising living standards in developing countries is the main driver of agricultural prices. Moreover, increasing urbanisation is contributing to a shortfall of farmland, which is slowing the closing of the supply gap. According to the Food and Agriculture Organization of the United Nations (FAO), droughts and floods could reduce worldwide crop yields by another 20% to 40% in future. To alleviate this looming food shortfall, the demand for modern farm machinery and irrigation equipment, efficient seeds, pesticides and fertilizers, aquaculture and suitable animal feed is likely to increase significantly. The investment concept of DJE - Agrar & Ernährung is to select companies that benefit from these trends. In the case of falling commodity prices the fund, can benefit from investments within the food sector. To reduce risk the fund seeks to diversify the portfolio both thematically and regionally.

Chances

- Active portfolio management constantly monitors the industry

- Risk spreading via the professional selection of securities

- Attractive growth prospects in the agriculture and food sector

Risks

- Issuer country and credit risks

- Increased risk of price fluctuations resulting from focus on specific sectors

- Equity prices may exhibit relatively strong fluctuations depending on market conditions

- Price risks for bonds, particularly when interest rates on the capital markets rise

Monthly Commentary

Although the US port of Baltimore is relatively insignificant for the trade of grain, negative effects on other important supply chains cannot be completely ruled out due to the collapse of the bridge there. For example, Russian nitrogen fertiliser shipments were imported into the USA via the port, as was potash fertiliser from Chile. Should the quantities now be sold elsewhere on the world market, this would undoubtedly make local fertilisers more expensive for US farmers there. An escalation of the Middle East conflict could also have an impact on global pricing, as the crisis region accounts for 50% of urea fertiliser exports. However, a large proportion of imported agricultural machinery and many production components also travelled via the port of Baltimore. Even if agricultural machinery manufacturers find replacement ports at short notice, delivery delays of up to 30 days must be expected. Accordingly, agricultural machinery manufacturers can certainly expect sequential shifts in sales and inefficiencies in the manufacturing process. In view of the additional supply chain problems mentioned above and the increasing geopolitical risks, fertiliser stocks are therefore still preferred in the fund. The shares of food additive suppliers could potentially benefit from the renewed formation of safety stocks among food producers.