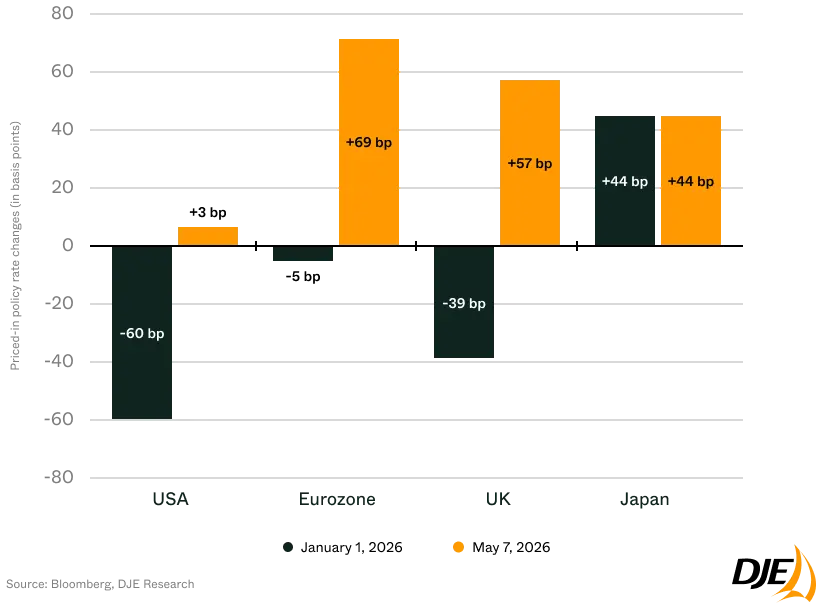

Expectations for monetary policy have shifted significantly within just a few months. At the beginning of 2026, investors largely anticipated that major central banks would deliver meaningful interest rate cuts over the course of the year. Declining inflation rates and hopes for an economic slowdown appeared to pave the way for a synchronized global easing cycle. That assessment has since been revised considerably.

The primary driver behind this reassessment is the renewed rise in inflation expectations. At the center of concerns is the geopolitical escalation in the Middle East. The conflict involving Iran and uncertainty surrounding the Strait of Hormuz — one of the world’s most critical oil shipping routes — have pushed energy prices sharply higher and intensified fears of another inflationary wave.

As a result, central banks are once again facing a policy dilemma. On the one hand, growth is weakening across parts of the global economy. On the other hand, higher oil prices threaten to keep inflation elevated for longer. Particularly concerning is the fact that energy price shocks often feed through with a lag into transportation costs, industrial prices and ultimately also into services and wages. Several central banks have already explicitly warned about such second-round effects.

The impact is already visible in market pricing. In many countries, expectations for substantial rate cuts have been scaled back significantly. In some cases, investors are once again even pricing in potential rate hikes. Expectations for a prolonged restrictive monetary policy stance have risen particularly in energy-dependent economies such as the euro area.

The chart therefore illustrates a fundamental shift in market sentiment. Instead of a synchronized global scenario characterized by falling interest rates worldwide, markets are increasingly focusing on a scenario in which geopolitical risks and structurally higher inflation continue to put pressure on monetary policy for an extended period of time.

Legal notice

Marketing Disclosure - All information published herein is for your information only and does not constitute investment advice or any other recommendation. The statements contained in this document reflect the current assessment of DJE Kapital AG. These may change at any time without prior notice. All statements made have been made with care in accordance with the state of knowledge at the time of preparation. However, no guarantee and no liability can be assumed for the correctness and completeness.