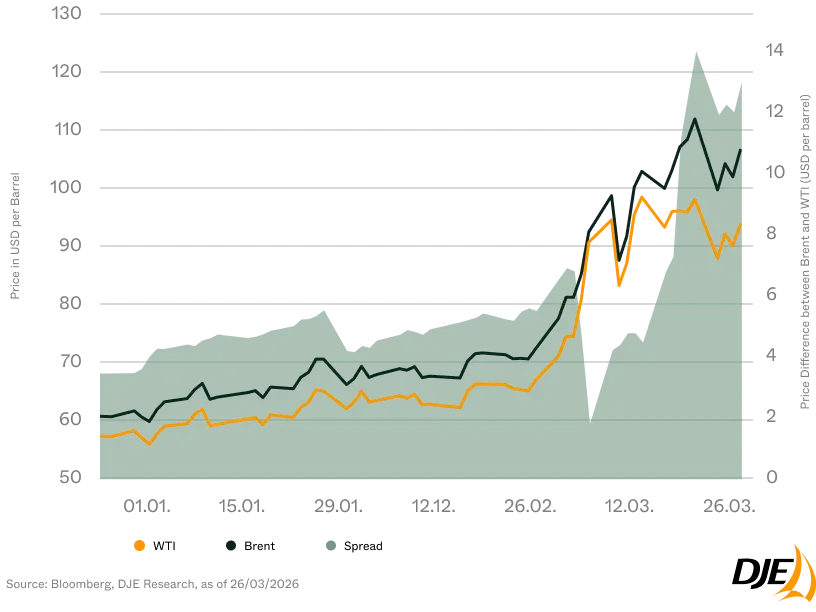

Oil is a globally traded commodity, but it is not homogeneous. Differences in quality, production region and logistics result in regional price differences. Of particular relevance are the two benchmarks Brent (North Sea) and WTI (West Texas Intermediate, USA), which together account for a large share of international oil price formation.

Historically, the price gap between Brent and WTI has typically moved within a range of around USD 2 to USD 5 per barrel. This difference mainly reflects transport costs, quality differentials and regional market structures. In periods of balanced supply and demand, the gap tends to remain relatively stable. At present, however, there is a clear departure from this pattern. The spread has recently widened at times to more than USD 10 per barrel – a level that points to structural tensions in the global oil market. While Brent, as the global benchmark, is more strongly influenced by international supply risks, WTI remains more closely tied to developments in the U.S. market.

A key driver is the geopolitical situation: production cuts by major producers and uncertainty in key export regions have tightened globally available supply. Brent reacts particularly sensitively to this, as it reflects the seaborne international oil market. At the same time, U.S. oil production has expanded significantly in recent years and currently stands at around 13 million barrels per day, close to historic highs. This development is the result of a long-term transformation: driven by the expansion of shale oil production and technological advances, the U.S. has evolved from one of the world’s largest importers into one of its most important producers and exporters. Since the lifting of the export ban in 2015, U.S. crude oil exports have risen to more than four million barrels per day.

The resulting relative self-sufficiency has a stabilising effect on the WTI price. Even in the face of global disruptions, supply in the U.S. market remains comparatively robust. At the same time, infrastructure constraints – such as limited pipeline or export capacity – can prevent excess supply from fully reaching the global market. This puts additional pressure on WTI.

The current spread is therefore more than a short-term market move. Rather, it shows that the oil market is becoming structurally more fragmented. While Brent reflects increasing scarcity and geopolitical risks in the global market, WTI stands for the growing resilience and production strength of the U.S. The oil market is thus becoming increasingly fragmented, and the gap between the two benchmarks is turning into an indicator of this new reality.

Legal information

Marketing advert: All information published here is for your information only and does not constitute investment advice or any other recommendation. The statements contained in this document reflect the current assessment of DJE Kapital AG. These may change at any time without prior notice. All statements made have been made with care in accordance with the state of knowledge at the time of preparation. However, no guarantee and no liability can be assumed for the accuracy and completeness of the information.