The debate around U.S. public debt is often accompanied by concerns that foreign creditors could retreat from the market for U.S. Treasuries, thereby jeopardizing the country’s funding capacity. In reality, however, the data have been pointing to a different trend for years.

To be sure, rising deficits, political standoffs over the debt ceiling and higher market interest rates caused bouts of unease in financial markets during 2025. Yet there was little evidence of a structural loss of confidence in capital flows. Demand remained robust for both U.S. equities - particularly large-cap technology stocks - and U.S. Treasuries.

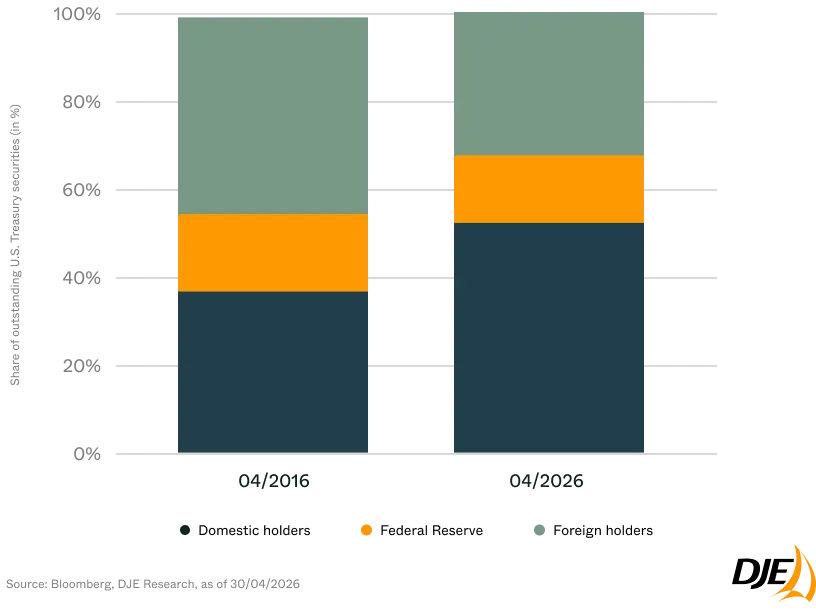

The long-term trend in the ownership structure of U.S. Treasuries reinforces this picture. Ten years ago, foreign investors accounted for around 45% of outstanding Treasuries. That share has now fallen to roughly one-third. At the same time, the role of domestic investors has increased significantly. Today, U.S. Treasuries are held primarily by American pension funds, insurance companies, banks, mutual funds and retail investors. Even as it reduces its balance sheet, the Federal Reserve remains a key player in the market.

This meaningfully challenges a widely used narrative: neither China nor Japan is truly decisive for the United States’ short-term funding capacity. Both countries remain important creditors, but their relative importance within the overall market has declined over many years. Owing to the size and depth of its capital markets, the U.S. continues to benefit from an exceptionally broad domestic investor base.

That said, this does not mean the debt trajectory is unproblematic. Public debt continues to rise, while both short- and long-term interest rates are materially higher than they were just a few years ago. As a result, the government’s funding costs are increasing noticeably. The key determinant of debt sustainability is therefore less the question of foreign buyers and more the path of nominal growth, productivity and inflation.

Legal information

Marketing advertisement - All information published here is for your information only and does not constitute investment advice or any other recommendation. The statements contained in this document reflect the current assessment of DJE Kapital AG. These may change at any time without prior notice. All statements made have been made with care in accordance with the state of knowledge at the time of preparation. However, no guarantee and no liability can be assumed for the correctness and completeness.